TABLE OF CONTENTS

DOWNLOAD: The Visualisation of the KPIT valuation in PPT format

1. Analysis Approach

We will evaluates company based on the following mechanisms:

- Rating System assigns a value of 0 for Neutral, 1 for Advantage, and 2 for Critical/Weighted.

- LPIs, which stands for “Legit Possibility Of Investment,” are chosen as competitors after filtering out those that doesn’t fall under Declining Business Performance, Revenue, Profits, High Debt Burden, Negative Earnings and Cash Flows, or Risk and Uncertainty.

2. At Glance

Stock code: KPITTECH (NSE)

Share price: 1,148.00 INR (25 August 2023)

Intrinsic Value: 262 INR (25 August 2023),

Book Value: 60 INR (2023) ~20x overpriced (is it justifiable?)

LPIs: Total 36 companies in India IT Sector Midsize Market Cap are potential competitor of KPIT Tech.

3. Company Highlights & Internals:

+1 Point justification on: Is KPIT Tech Debt free and Is each share piece is under Intrinsic Value?

KPIT is a global technology company with software solutions that will help mobility leapfrog towards autonomous, clean, smart and connected future. With 10000+ Automobelievers across the globe, specializing in embedded software, AI & Digital solutions, KPIT enables customers accelerate implementation of next generation mobility technologies . With development centers in Europe, USA, Japan, China, Thailand and India.

- Market Capitalisation: 31,459 CR

As of August 2023, KPIT is trading at Stock(Price-to-Earning) at ~72x and and Stock(Price-to-book) at ~20x

Is KPIT Tech Debt free?: Yes, with 286.53 CR in debt with very minimal compared to the Market cap (1 point)

Is KPIT Tech currently under Intrinsic Value? No, with close to double of industry median PE and PB — KPIT can be identified as Overvalued at the moment (0 point)

Excerpt: There are overall 177 out off 240 debt-free Companies in India IT Sector Midsize Market Cap. Hence it seems less convoluted to be debt free in Software Industry.

3.a) Business Activities

KPIT Technologies is a leading player in the automotive technology domain, specializing in software solutions for Electric Powertrain, ECU (Electronic Control Unit), and Software-Defined Vehicles (SDVs). The company has recently secured a significant multi-million-dollar engagement with a prominent European Car Manufacturer in the Electric Powertrain domain, with a deal value exceeding $50 million. KPIT has also been chosen as a key partner by a leading European OEM for the next generation ECU, and Renault Group has recognised KPIT as a strategic technology partner.

KPIT’s business model is aligned with the transformation of the automotive industry towards Software-Defined Vehicles (SDVs). SDVs shift the concept of automobiles from one-time purchases to recurring revenue generation through software-driven features and services. The company’s growth is driven by its contributions to making vehicles more intelligent, responsive to the environment, and sustainable.

Competitors:In the automotive technology landscape, KPIT’s competitors include ESR Labs, which was acquired by Accenture Solutions in 2020.

3.b) Advantage & USPs

+1 Point justification on: Whats the scope of business scalability by 10x?

- Long-Term Evolution: SDVs provide a platform for ongoing innovation and evolution. As technology advances and new capabilities emerge, software updates can continuously enhance vehicle features and performance, extending the useful life of the vehicle.

- Rapid Feature Deployment: Traditional vehicles often require physical changes or updates to introduce new features. SDVs can receive software updates over-the-air (OTA), allowing manufacturers to rapidly deploy new functionalities and improvements without requiring a physical visit to a service center.

- Fleet Management and Logistics: In commercial applications, such as ride-hailing services or delivery fleets, SDVs can enable more efficient fleet management, route optimization, and driver monitoring, leading to cost savings and improved logistics.

- Holistic Solutions: KPIT offers a comprehensive range of solutions categorized into Feature Development and Integration, Architecture and Middleware Consulting, and Cloud-based Connected Services. This diverse portfolio enables the company to address a wide spectrum of client needs.

- Market Leader in SDVs: KPIT leads in providing cutting-edge software solutions for the Software-Defined Vehicle revolution. KPIT’s innovative contributions drive the industry’s transition towards intelligent and sustainable mobility.

Whats the scope of business scalability by 10x? KPIT’s position as a global market leader, with handful of player as direct competition, combined with its adaptable solutions, innovative prowess, and strategic partnerships, positions it well to achieve a significant 10x business scalability — (1 point)

3.c) Geographical Distribution & Opportunities

+1 Point justification on: Is there a possibility of 10x geography expansion for 20x revenue?

Revenue Dissection:

In the fiscal year 2022, KPIT Technologies achieved a balanced revenue distribution across global regions, with 39% from the USA, 40% from Europe, and 21% from the rest of the world. The revenue by verticals reflected its expertise, with 74% from passenger cars, 24% from commercial vehicles, and 2% from other sectors.

The revenue was strategically divided by practices, comprising 37% from powertrain, 19% from AD-ADAS, 11% from connected vehicles, and 33% from other areas. This comprehensive revenue split highlights KPIT’s global presence, adaptability across verticals, and strategic focus on distinct automotive technology practices.

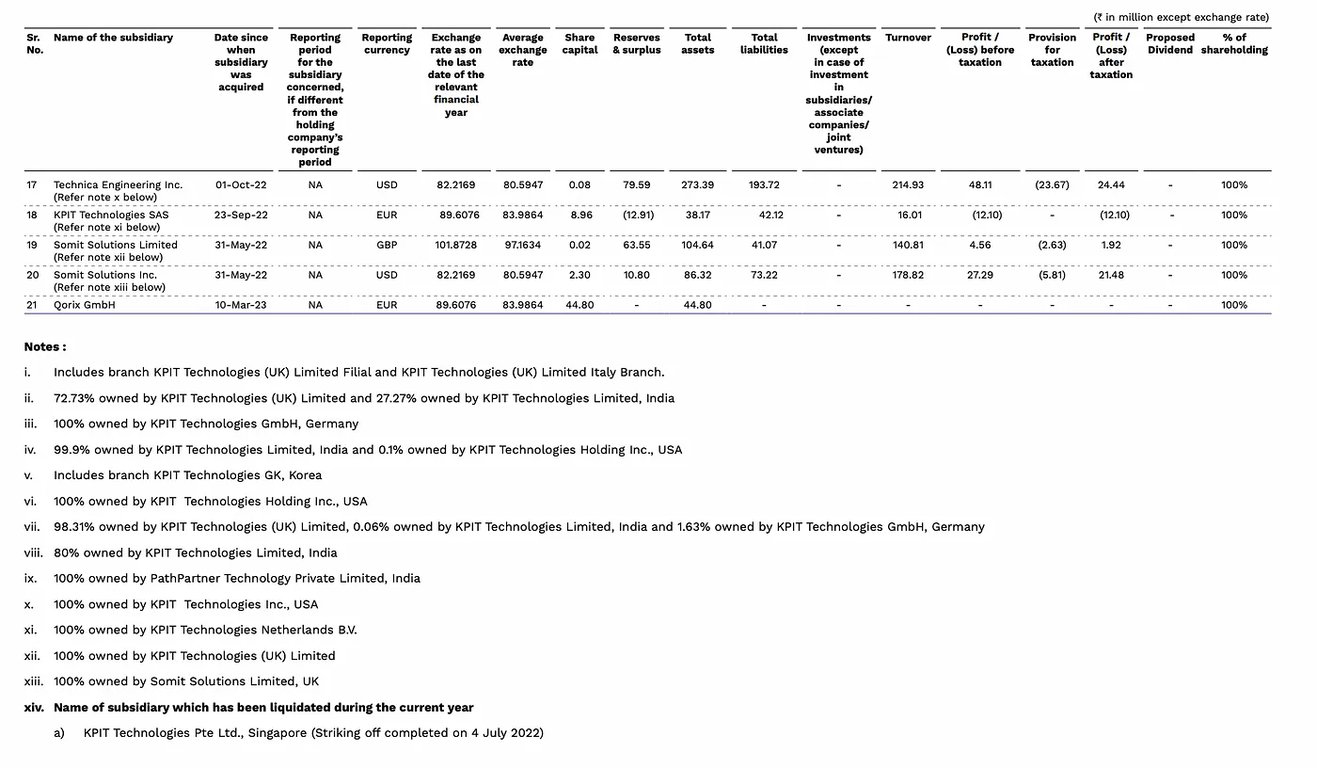

Global Subsidiaries:

KPIT Technologies operates with a dynamic network of subsidiaries, totalling 21 and accompanied by 1 associate company as of March 31, 2023. Strategically spread across diverse regions, these subsidiaries bolster KPIT’s expansion strategies and enhance its global impact. With a footprint in locations such as the UK, China, Netherlands, Germany, and the US, these subsidiaries bring specialized expertise to the table, contributing to the development of advanced solutions in domains like software-defined vehicles, autonomous driving, and connected services.

KPIT Growth Prospects:

- Early Mover Advantage: As an early entrant into the software-defined vehicles (SDV) space, KPIT enjoys a distinct advantage. This advantage stems from being ahead of the curve in terms of understanding the intricacies of SDV technology, regulatory frameworks, and market dynamics.

- Complex SDV Landscape: The landscape of SDVs is marked by its complexity, where software becomes the cornerstone of vehicle functionality. Traditionally, hardware constituted the majority of a vehicle’s cost, with software playing a secondary role. However, in SDVs, the equation is dramatically reversed, with software accounting for around 70% of the total vehicle cost. This shift necessitates a fundamental transformation in the automotive industry’s approach, from manufacturing-oriented to software-centric.

- Strategic Client Relationships: KPIT places considerable emphasis on fostering strong relationships with its top 25 clients (T25). This strategic approach not only enhances client loyalty but also facilitates collaborative innovation.

- Prominent Partnerships: Partnering with prominent automotive players like Honda and Renault Group underscore KPIT’s commitment to aligning its vision with the strategic goals of its clients. The collaboration with Honda for software-defined mobility (SDM) and the selection by Renault Group as a strategic partner for scaling software in their next-generation SDVs showcase KPIT’s significance in the industry’s value chain.

- Global Expansion: KPIT’s expansion strategy encompasses key global regions. While Europe and the USA remain primary focus areas, the company anticipates rapid growth in India and China. These two Asian giants are poised to contribute over 50% of global growth, as indicated by the International Monetary Fund (IMF). The alignment of KPIT’s growth trajectory with the growth potential of these markets enhances its chances of tapping into new opportunities and expanding its footprint significantly.

SDVs Industry Outlook:

- Total market cap for SDVs account for $35.72 billion

- Its expected to grow with CAGR of 19.2%

Is there a possibility of 10x geography expansion for 20x revenue? With forecast of SDVs industry and KPIT streak of M&A in last 5 years provide positive outlook — (+1 point)

4. Research & Development, and Patents

+2 Weighted points justification on: Is company headed in right direction toward broader horizon for future technology with precise R&D?

The company prioritizes Research and Development (R&D) as a technology-intensive organization. They’ve developed a cloud-based test automation platform for integrated system testing. With approximately 45 patents filed and four granted in FY22, they demonstrate a strong commitment to innovation.

These patents span under following areas:

- Advanced Driver Assistance Systems (ADAS) Technology: A significant portion of the patents, 18 in total, are related to ADAS technology, indicating a strong presence and commitment to advancing safety and automation in the automotive sector.

- Sentient Projects: The company has filed 9 patents related to Sentient projects, which may include innovative projects in artificial intelligence, machine learning, or other advanced technologies.

- Battery Management Systems: 3 patents are related to Battery Management Systems, signaling an interest in improving the efficiency and performance of electric and hybrid vehicles.

Following are the granted patents:

- JP 7064303 (Japan): Autonomous system validation.

- US 16252666 (U.S): System and method for detecting a vehicle in nighttime.

- IN 396297 (India): Torque assist for motor.

- IN 422731 (India): System and method for target track management of an autonomous vehicle.

Is company headed in right direction toward broader horizon for future technology with precise R&D? The company’s focused R&D efforts, evident through their innovative projects and patents, suggest they are heading in the right direction towards future technological advancements — Positive (+2 point)

5. Promoters, Management, & Employees

+1 Point justification each on: Does the Promoter really believe in the company? and Does Company has culture which promotes growth?

KPIT was co-founded in 1990 by Ravi Pandit and Kishor Patil

Ravi Pandit was previous CEO of KPIT Tech. He has been honored with the Maharashtra Corporate Excellence (MAXELL) Awards for Excellence in Entrepreneurship and for his contribution to the economic and industrial development of Pune City.

Kishor Patil, who assumed the role in January 2019, has been in the position for approximately 4.67 years. His annual compensation totals ₹46.43 million, with 26.1% attributed to salary and 73.9% to bonuses, which include company stock and options.

Few Excerpt:

- He was awarded Best CEO of the Year by ET Ascent in collaboration with HRD Congress. From Industry Partners

- Notably, he holds a direct ownership stake of 4.93% in the company, valued at ₹16.02 billion.

The management team and board of directors, on average each have a tenure of 4.7 years.

Promoter Shareholding:

Promoters have maintained a stable holding in the company, with their ownership ranging from 39.47% to 41.65% over the past five periods. This indicates a consistent level of control and involvement in the company’s affairs.

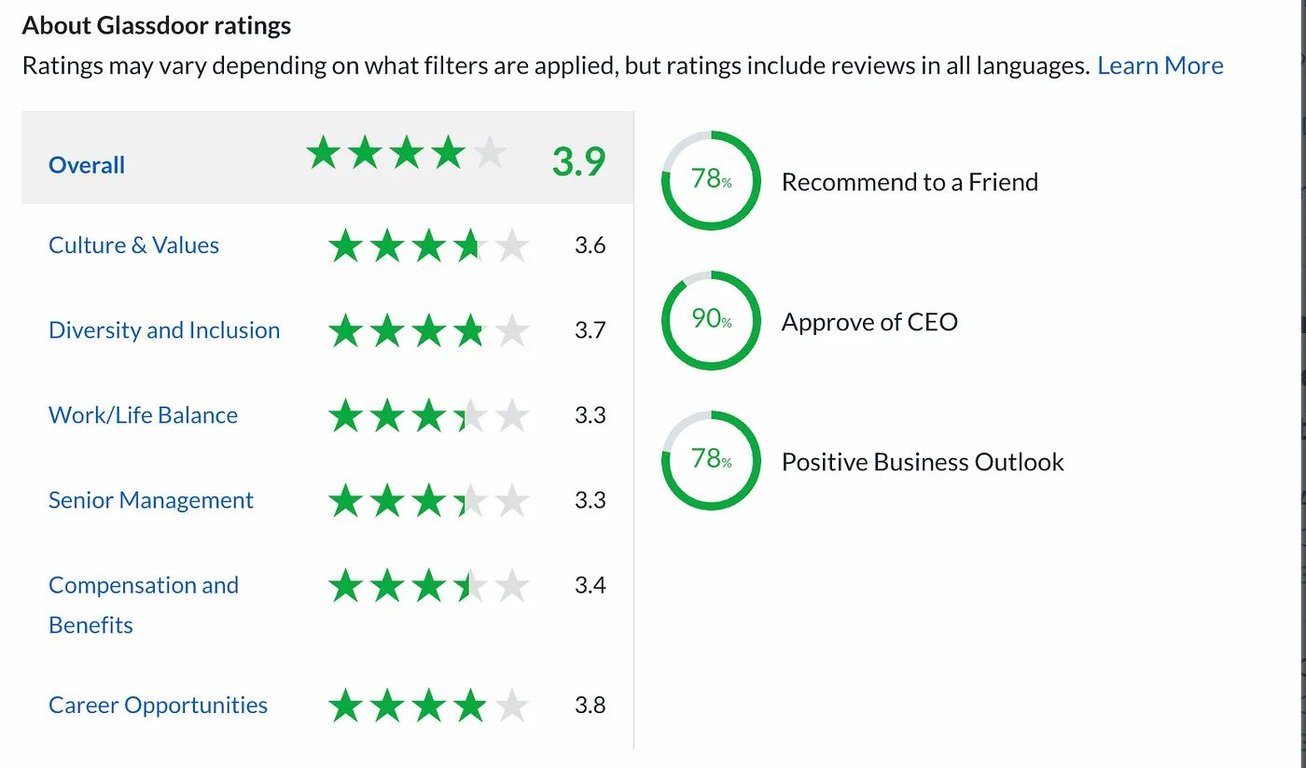

Operational Employee Attitude:

The feedback provided on Glassdoor has positive sentiment.

- This rating has improved by 6% over the last 12 months.

- 3.3 out of 5 for work life balance

- 3.6 for culture and values and

- 3.8 for career opportunities.

Does the Promoter really believe in the company? The Promoter’s substantial ownership stake in the company and their consistent holding suggest a strong belief in KPIT Technologies. — (+1 point)Does Company has culture which promotes growth? The above average employee sentiment on Glassdoor, with high recommendations and improved ratings, indicates a company culture that promotes growth and a favorable work environment. . — (+1 point)

6. Return On Equity & Return On Capital Employed

+2 Weighted points justification each on: KPIT (Challenger) ROE of 5 years vs Inflation, and Industry? and KPIT (Challenger) ROCE of 5 years vs Industry?

ROE of 5 years vs Inflation, and Industry?

- The Indian Economy average ROE in the last 3 years is 10.06%, while maximum inflation in the last 5 years which was 6.62%.

- Route mobile comes on Rank 32 compared to LPIs with ROE of 22.5%, 20.73%, and 19.34% in Preceding year, Last 3 years average, and Last 5 years average.In comparison, the best in this zone is Tata Elxsi — which has 37%, 36%, and 34%.

- The average ROE for 55 companies under LPIs is 22.37%.

ROCE of last 5 years vs Industry?

Return on capital employed is a financial ratio that measures a company’s profitability in terms of all of its capital.

- ROCE of KPIT Tech in last year, average 3 years and average 5 years has been 24.8%, 24.9% and 19.85%.

- Industry Average ROCE for LPIs in last year, average 3 years and average 5 years has been 21%, 25.10%, and 24.34%.

KPIT Tech (Challenger) ROE of 5 years vs Inflation, and Industry Average? KPIT Tech is aligned with average ROE of quality competitor s— Positive (2 Points)KPIT Tech (Challenger) ROCE of 5 years vs Industry Average? Above number definitely provides insight that ROCE justified in comparison to industry is consistently above average — Positive (2 Points)

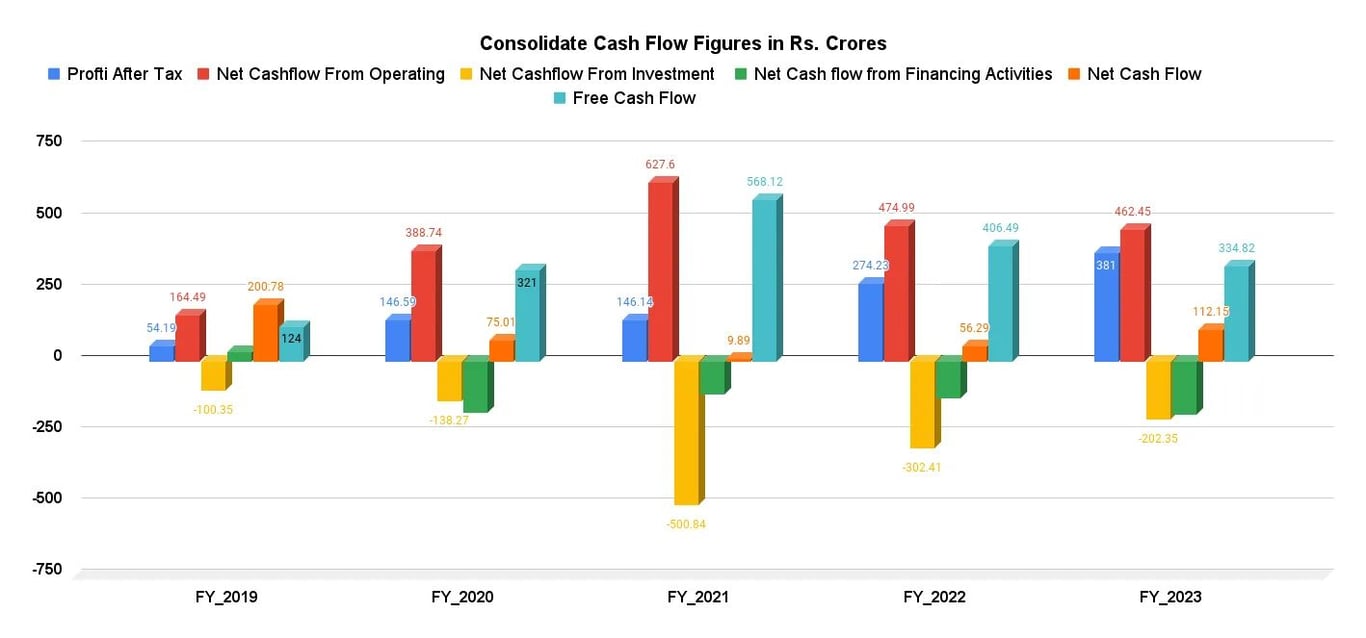

7. Cash flow Analysis:

+1 Point justification each on: Is the Net Cashflow (Standalone & Consolidated) consistently positive? Is the Cashflow from Operating Activity (Standalone & Consolidated) is consistently positive? Is the CFO:PAT converging in alignment consistently for last 5 years?

The above cashflow chart depicts Consolidate Operating Cashflow is in better position compared to Standalone Operating Cashflow.

Is the Net Cashflow (Standalone & Consolidated) consistently positive? However the Net Cash Flow has not been consistently positive over the last five years. It fluctuated between positive and negative values during this period.— Neutral (0 point)Is the Cashflow from Operating Activity (Standalone & Consolidated) is consistently positive? The Cashflow From Operating Activity has been consistently positive over the last five years, indicating that the company generated positive cash flow from its core operations.— Positive (1 point)

The CFO:PAT ratio is not consistently converging but rather fluctuating over the five-year period. It appears to have increased significantly in FY 2021 and then decreased in subsequent years. This suggests some variation in the alignment of cash flow from operations to profit after tax over the years.

the average CFO/PAT ratio for KPIT Technologies over the last five years is approximately 2.58

Is the CFO:PAT converging in alignment consistently for last 5 years? The average CFO/PAT ratio for KPIT Technologies over the last five years is approximately 2.58. This healthy Profit After Tax to CFO ratio is considered a positive sign for investors and stakeholders, as it reflects the company’s ability to manage its finances efficiently and generate sustainable cash flow — Positive (1 point)

8. Other Financials

+1 Point justification each on below 5 matrix

1.) KPIT Tech dividend yield is 0.36% but significantly lower compared to the average LPIs which (0.75%), indicating a relatively modest dividend yield position —Neutral (0 point)

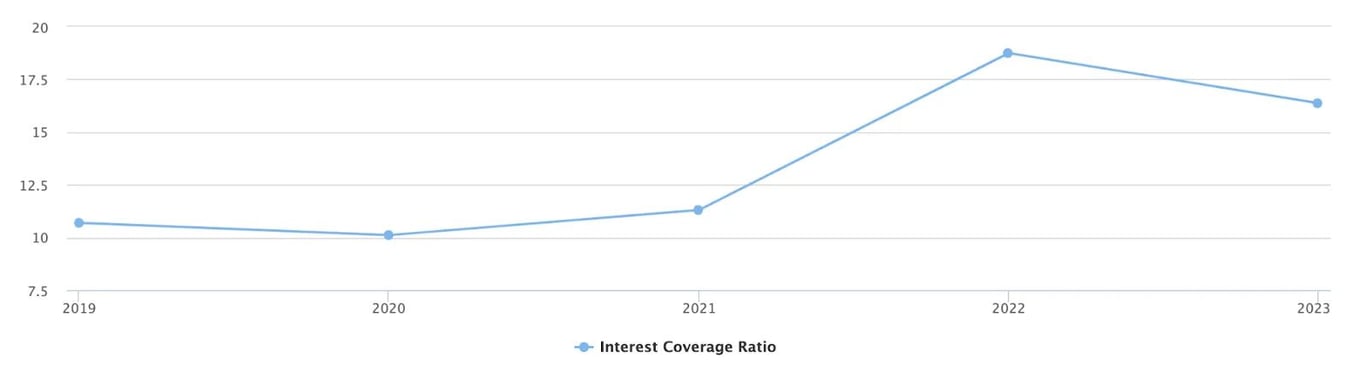

2.) The Interest Coverage Ratio is a healthy 15.22, hence positive — (1 point)

— A ratio of 15.22 suggests that KPIT Tech operating profits are 19.7 times higher than its interest expenses, indicating a strong financial position.

— The last 5 years average is also quite healthy.

3.) KPIT Technology 5-year average OPM (%) is approximately 16.67%, while the LPIs’ average is 18.94%, hence below LPIs average — (0 points)

— A lower OPM than the industry average might suggest potential areas for cost optimization or efficiency improvement, and which may require further examination to understand the reasons behind this trend.

4.) Debt-to-Equity Ratio of KPIT Tech hasn’t gone over 0.2, positive — (1 point) KPIT Technologies maintains a solid balance sheet, with manageable debt and a net cash position.

5) Sales growth averages for the last 3 years and 5 years are 16% and Nil%, respectively, surpassing the industry LPI average of 22% and 18%, hence Neutral — (0 point)

— KPIT has achieved acceptable sales growth over both short-term and incomparable long-term (5 year) periods due to change in their business process.

9. Closure

Category | Count | Details |

Total Points Analyzed | 18 | ㅤ |

Points in Favor of Investing | 10 | 1. Debt-Free Status: Minimal debt compared to market capitalization. |

ㅤ | ㅤ | 2. Scalability Potential: Potential for business scalability by 10x. |

ㅤ | ㅤ | 3. Innovation Commitment: Strong commitment to R&D and patents. |

ㅤ | ㅤ | 4. Promoter Belief: Positive company culture and promoter’s belief in the company. |

ㅤ | ㅤ | 5. Healthy ROE: Healthy Return on Equity compared to inflation and industry. |

ㅤ | ㅤ | 6. Above-Average ROCE: Above-average Return on Capital Employed compared to the industry. |

ㅤ | ㅤ | 7. Positive Cash Flow: Consistently positive Cash Flow from Operating Activities. |

ㅤ | ㅤ | 8. Geographical Expansion: Potential for 10x geographical expansion and revenue growth. |

ㅤ | ㅤ | 9. Consistent Ownership: Promoter’s consistent ownership stake without significant changes. |

ㅤ | ㅤ | 10. Favorable Employee Sentiment: Employee sentiment reflecting a favorable work environment. |

Neutral Points | 3 | 1. Overvaluation: Stock trading at a high Price-to-Earnings (P/E) and Price-to-Book (P/B) ratio. |

ㅤ | ㅤ | 2. Fluctuating Cash Flow: Cash Flow from Operations and Net Cash Flow fluctuating over the last five years. |

ㅤ | ㅤ | 3. Operating Margin Growth: Operating Margin (%) growth slightly below LPIs. |

Negative Point | 1 | 1. Stock Overvaluation: Highlighting the overvaluation of KPIT Technologies’ stock. |

Overall, the analysis suggests that KPIT Technologies has several positive attributes, including strong fundamentals, innovation potential, and financial stability.

In conclusion, KPIT Technology seem to have lucrative investing opportunity but currently overvalue, right price to invest in this wonderful growing business will be around 2x of Intrinsic value. Suggestion is to wait for next 6–12 months for prices to fall below 750 INR.

Related Posts

Made with Bullet

Made with Bullet